Have you ever wondered how South Carolinians paid for goods and services before the advent of the U.S. dollar? The pound sterling formed the basis of their accounts until the 1790s, but the economic realities of frontier life obliged early Carolinians to embrace monetary tools and strategies that deviated from British traditions. For more than a century, inhabitants of the Palmetto State used foreign coins, paper bills, promissory notes, and sophisticated credit schemes that fueled upward mobility and set the stage for the financial systems we use today.

My goal in this program is to provide an accessible overview of a complex topic, and to help people understand how our forebears rendered payment for expenses large and small, from buying a drink in a tavern, or an enslaved person at auction, to purchasing a large plantation or townhouse. The mechanisms and methods behind such transactions in colonial-era South Carolina were once more complicated than you might realize, and demonstrate that our predecessors acquired an impressive degree of financial literacy.

The present City of Charleston was founded in 1670 as the capital of an English colony chartered as an elaborate business venture. Its primary purpose was to generate wealth for its principal investors, the Lords Proprietors of Carolina, and for subsidiary investors in England and on the ground in Carolina. For more than a century, South Carolina functioned as an economic, political, and cultural satellite of England and then Great Britain (after its union with Scotland in 1707). Like other British colonies around the globe, the commercial relationship between Carolina and the mother country was defined by an economic construct we now call mercantilism. That is to say, the satellite colonies provided relatively cheap raw materials and commodities that enhanced the economy of Great Britain, which in turn generated valuable manufactured goods and luxury items that were exported to the colonies. This purposefully lopsided economic relationship created a trade imbalance that kept the colonies in state of perpetual dependence until the coordinated rebellion of 1775.

The early residents of South Carolina and other Anglo-American colonies kept track of their wealth using the pound sterling (£) as the basis of their accounts, just like their contemporaries in England, with one major difference. While the residents of Great Britain used coins made of gold, silver, and copper denominated in pounds, shillings, and pence, government trade policies discouraged the flow of such coins—called “specie”—to the colonies. There were no banks in South Carolina until after the American Revolution, and the British government never authorized the minting of specie in its overseas colonies. A relatively small volume of English coins did migrate to the colonies with settlers and traders, but, owing to the perpetual trade imbalance, most of those coins soon returned to the mother country in the form of payments for goods received from Britain. In the context of this scarcity of money, the residents of South Carolina and other colonies had to embrace alternative forms of exchange not shared by their contemporaries in Britain.

At the local level, early settlers migrating to the Lowcountry of South Carolina used the timeless practice of bartering for goods and services among themselves and with the sparse Indigenous population that once inhabited the region. One might casually negotiate the exchange of shrimp for an axe, for example, or agree to build a fence in exchange for a certain number of deerskins. Larger transactions based on commodities required more complex accounting, however, including a schedule of prices that reflected the conditions of a specific time and place.

In response to these conditions, South Carolina’s provincial government ratified several laws in the 1680s and 1690s to establish the price of bulk commodities like deerskins, rice, and wood products, and thereby facilitate commerce. The proliferation of trade between the colonies and across the Atlantic in the eighteenth century produced a greater pool of data about commodity prices near and far, resulting in more robust price indexes. Country planters and merchants adjacent to the wharves of Charleston were always eager to know the latest commodity prices, even before the colony’s first newspaper, the South Carolina Gazette, began printing a weekly table of “prices current” in 1732.

Let’s consider a simplified version of a real-world transaction to illustrate how colonists conducted business without the use of cash. A planter in colonial South Carolina, for example, might deliver a crop of rice to a merchant in Charleston and negotiate its sale. Based on the total volume of the rice and the latest known price of bulk rice on trans-Atlantic market, the merchant would offer a sum to the planter for his crop. If the planter accepted the bargain, he or she did not receive cash in hand, but rather credit rendered in pounds, shillings, and pence. The planter could then redeem such credit to purchase supplies like tools, provisions, animals, and even enslaved people—depending on the commercial scope of the merchant in question.

Similarly, the Charleston merchant who shipped Carolina produce to England received overseas credit rather than cash payment for the goods in question. He or she could spend that credit in South Carolina by creating a simple written document called a “bill of exchange” that functioned very much like a modern check (or cheque). Likewise, the merchant in Charleston selling goods imported from London could render cash-less payment to his supplier by sending overseas a bill of exchange linked to credit held in England by a relative or business partner or another merchant. In each of these scenarios, which I’ve simplified for the sake of clarity, frontier residents of colonial South Carolina conducted business and accumulated wealth without the use of traditional cash.

The abstract notion of remote credit served the needs of planters and merchants engaged in trans-Atlantic and inter-colony trade, but their bills of exchange were too cumbersome for use in smaller transactions made at the local level. To facilitate buying and selling within a community like Charleston, colonists sought a medium of exchange—that is, a form of cash-in-hand—with a recognized and relatively stable value. The initial answer to this need came not from the English government in London, but from the agents of competing nations circulating in other parts of the New World.

South Carolina’s proximity to the Caribbean Sea meant that a significant proportion of its early trade flowed southward to British ports in the Bahamas, Antigua, Barbados, Jamaica, and other islands. Maritime trade—legal and illegal—with Dutch, Danish, French, Portuguese, and Spanish agents in the Caribbean infused a significant volume of foreign coins into the Anglo-American economy. Some of that foreign specie flowed northward to Charleston and beyond, where settlers were eager to have what was often called “ready money” with which to conduct business.

The most common foreign coins in colonial Charleston were Spanish dollars, or pieces of eight, which were minted from silver extracted from mines in Mexico and Peru. Because the practice of clipping and filing the edges of such coins often reduced their value, Anglo-American colonists cultivated a habit of weighing Spanish dollars and other foreign specie and assigning to them a value in comparison to British pounds sterling. For the entirety of South Carolina’s colonial period, merchants in London valued a full-weight Spanish dollar at four shillings and six pence (£0.4.6), or 54 pence, sterling.

Foreign coins served as the “current money” of late seventeenth century colonial America, where merchants offered higher rates of exchange than in England to encourage the coins to remain in local circulation. South Carolina’s early provincial legislature, like that of other colonies, ratified laws to establish the local overvalue of foreign coins, and competition between the colonies caused their value to increase significantly. To check this inflationary trend at the beginning of the eighteenth century, Queen Anne issued a proclamation to settle the maximum overvalue of the ubiquitous Spanish dollar, which proclamation was reinforced by an act of Parliament in 1708. For the remainder of the eighteenth century, British law dictated that the value of a full-weight Spanish dollar in the American colonies was equivalent to six shillings (72 pence) sterling. Colonists routinely ignored this limitation in their private transactions, but government documents of the eighteenth century contain occasional references to so-called “Proclamation money” as the preferred method of rendering public payments like taxes, import-export duties, and court fees. Proclamation money was not a distinct type of currency or coin, therefore, but simply a fixed ratio expressing the relative value between British sterling and the Spanish dollar that applied only to transactions made in the American colonies.

Spanish and other foreign coins continued to circulate in Charleston beyond the era of the American Revolution, but their use was partially eclipsed by the introduction of a new medium of exchange at the turn of the eighteenth century. Beginning in 1703, South Carolina’s provincial government began “emitting” paper money in various denominations that quickly became a significant form of “current money” in the colony. These ephemeral monetary instruments, known as “bills of credit,” were simply rectangular pieces of paper stamped with a novel design engraved by a local artisan. To discourage counterfeiting, each bill was signed by the several commissioners appointed by the provincial government to manage the fund. These commissioners, in concert with the colonial legislature, limited the volume and lifespan of the bills to control their value in relation to British sterling.

The paper bills of colonial-era South Carolina were denominated in traditional English units (that is, 12 pence in the shilling, and 20 shillings in the pound), but they always represented a fractional value in relation to sterling money. The earliest paper currency printed in Charleston in 1703 was valued at one third less than sterling, meaning that one and a half South Carolina pounds (or 30 shillings) were equal to one English pound sterling (20 shillings). The convenient utility of this paper medium fueled the expansion of the provincial economy during the early years of the eighteenth century and inspired the South Carolina legislature to authorize further emissions and to keep the bills in circulation for longer periods than originally intended. These controversial actions, combined with economic setbacks like the Yemasee War of 1715–17, the pirate troubles of 1718, and the Revolution of 1719, gradually eroded the value of the paper bills until it reached the ratio of seven South Carolina pounds to one pound sterling in the late 1720s. Following the British Crown’s purchase of the Carolina colony from the Lords Proprietors in 1729, the value of South Carolina’s paper currency remained stable at or very near the ratio of 7:1 until the early days of the American Revolution.

South Carolina’s provincial government did not issue a continuous stream of paper money after 1703; rather, officials released a significant quantity of bills in discrete batches at irregular intervals over multiple decades. These successive emissions produced paper bills in different volumes and in different denominations that were intended for different purposes and backed by different redemption schemes. Some were simply fiat money—backed by no security—while others were more like bearer bonds with a redeemable value. Many were produced to fund specific building campaigns, much like a modern municipality might issue bonds to fund the construction of a library or a highway.

In 1767, for example, the South Carolina General Assembly ratified an act to raise “sixty thousand pounds current money of this province” (equal to £8,571 sterling) for the construction of a new Exchange building that still stands at the east end of Broad Street in Charleston. The law empowered a group of commissioners to print and sign three thousand paper bills called “public orders,” each valued at £20 pounds in South Carolina currency, which they used to pay contractors hired to supply materials and labor for the project. The design of the bill included a printed statement empowering the bearer to use it to pay taxes or duties due to the provincial government at any point before an expiration date in 1772. These three thousand paper bills, each of which featured a small illustration of the proposed Exchange building, circulated as a medium of exchange for a maximum of five years before bearers returned them to the government as tax payments. The commissioners were required, as usual, to burn the returned bills, but a few have survived in archival collections.[1]

In addition to the limited volume of foreign coins and paper bills circulating in early South Carolina, residents also conducted a significant proportion of their day-to-day commerce using credit rather than cash. To buy a drink in a tavern or a loaf of bread from a baker, for example, one might hand over a silver coin or a paper bill issued by the provincial government. Odds are, however, that the value of such coin or bill is greater than the cost of several drinks or loaves of bread. If one is a regular customer, the proprietor might record your purchase as a debit in his business ledger and expect you to render payment at some point in the future. This sort of small-scale credit, known as book debt, was extremely common in early South Carolina and elsewhere in the American colonies, where cash was scarce and one’s personal reputation counted as a valuable asset.

Many people of that era, including plantation owners, ship captains, ministers, teachers and civil servants, experienced long and often irregular intervals between payments for the goods and services they rendered. After waiting a year or more for their dividends or salaries, they might perambulate through the streets of urban Charleston to settle several years’ worth of book debts in a single day. One can imagine, for example, that a widowed plantation owner might use the latest price index to calculate the approximate value of a crop of rice shipped to England by a Charleston merchant or factor working on commission. She might then visit a tailor and a seamstress in the capital to commission new clothes for her family and servants, visit a wine merchant to have casks of claret sent to her country estate, select a fancy new carriage from a local coachmaker, and browse a bookshop to select new volumes for her personal library. At each of these stops, this hypothetical widow could leverage her reputation in the community to secure credit from several individual proprietors, each of whom kept ledgers of book debt incurred by scores of similar customers. If the widow’s crop fetched a good price in England, she or her agent might retire her various debts in a single blow. If the crop fell short, however, she might beg her creditors for patience and continue accruing debt leveraged against next year’s harvest. A handful of extant business ledgers recorded by eighteenth-century merchants like Henry Laurens help us understand the pervasive use of personal credit in early South Carolina. Similarly, the records of civil lawsuits and probate inventories demonstrate that many small-scale merchants, including vintners, shopkeepers, and artisans, often waited years and even decades for customers to clear their outstanding debts.

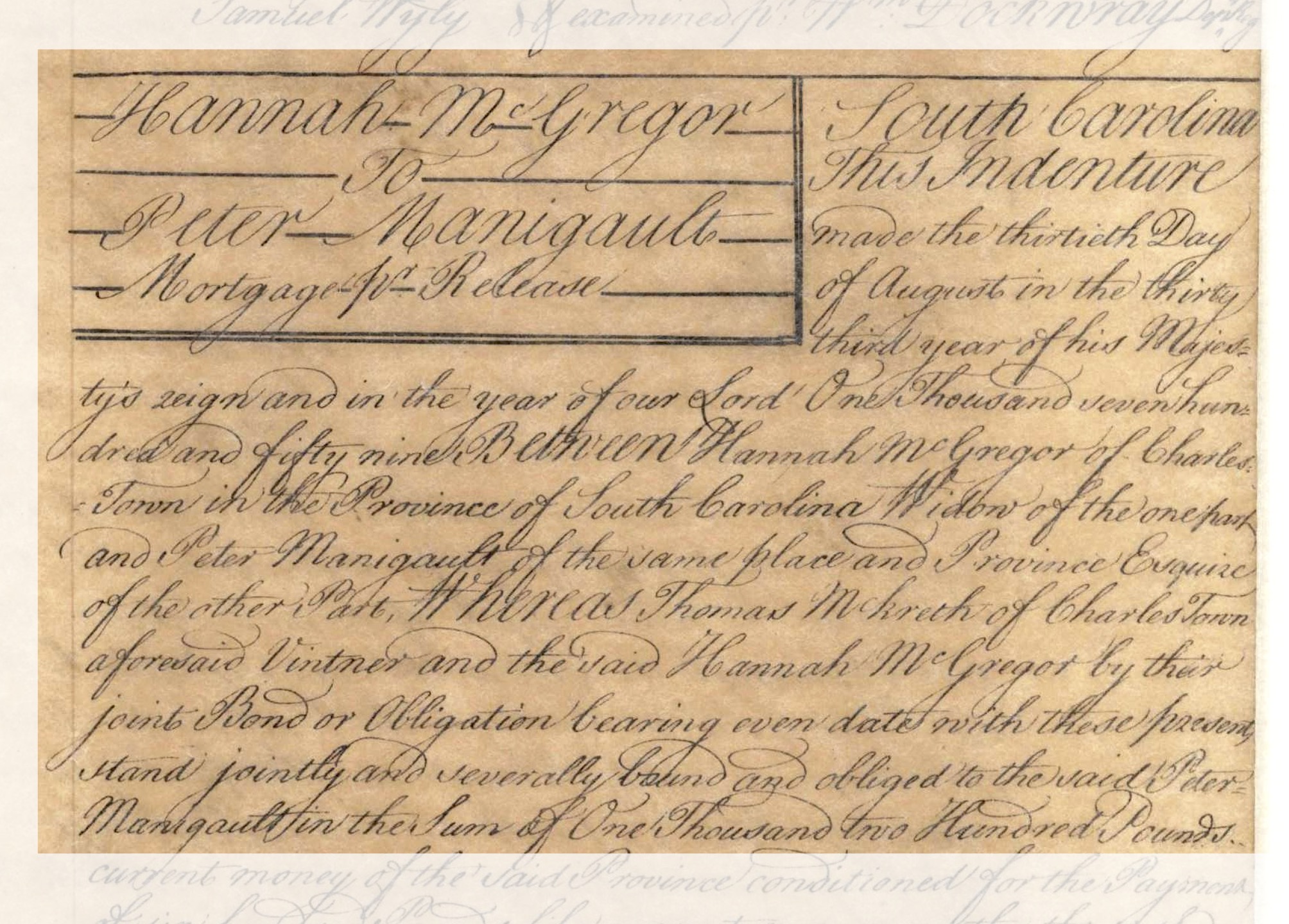

Although there were no banks in colonial-era South Carolina, numerous residents expanded their personal wealth by obtaining mortgages. A mortgage, after all, is simply an extension of credit, the repayment of which (with interest) is secured against some form of property, either real (i.e., land) or chattel (i.e., moveable). A plantation owner, for example, might mortgage their land to a relative or frenemy to purchase additional acreage. A baker, or carpenter, or similar tradesperson might purchase their first house by obtaining a short-term mortgage on the property from its current owner (like a rent-to-own scheme). Additionally, a slave owner could mortgage their human chattel to a slave broker to secure credit used to purchase more slaves, then use their collective labor to satisfy the debt and repeat the process over and over to amass a fortune. Anyone wishing to explore these kinds of financial strategies will find hundreds of colonial-era land mortgages recorded among the property records archived by the Charleston County Register of Deeds, and thousands of early chattel mortgages among the voluminous records of the Secretary of State at the South Carolina Department of Archives and History in Columbia (SCDAH).

Credit cards, which modern shoppers use to accumulate unsecured debt, did not exist in colonial America, but a very similar instrument was available to adults with established reputations. An eighteenth century South Carolinian could purchase items of significant value—like a harpsichord, a carriage, a ship, a house, or enslaved people—using a personal bond, which was essentially a formal promissory note pledging repayment (with interest) over a specified period of time ranging from a few months to a few years. In the absence of banks, merchants and individuals with stores of credit or cash reserves often extended such unsecured loans to their friends and trusted customers. A bond was a legally-binding contract, and failure to repay the sum within the specified timeframe could result in a lawsuit. Most extant bonds from eighteenth-century South Carolina include verbiage stating that the borrower was liable to pay a “penal sum” double the value of the original loan if he or she failed to satisfy the terms of the agreement. Thousands of personal bonds can be found among the aforementioned records of the Register of Deeds and the Secretary of State, and among the extant records of South Carolina’s early Court of Common Pleas, which you’ll find at the state archive (SCDAH) in Columbia.

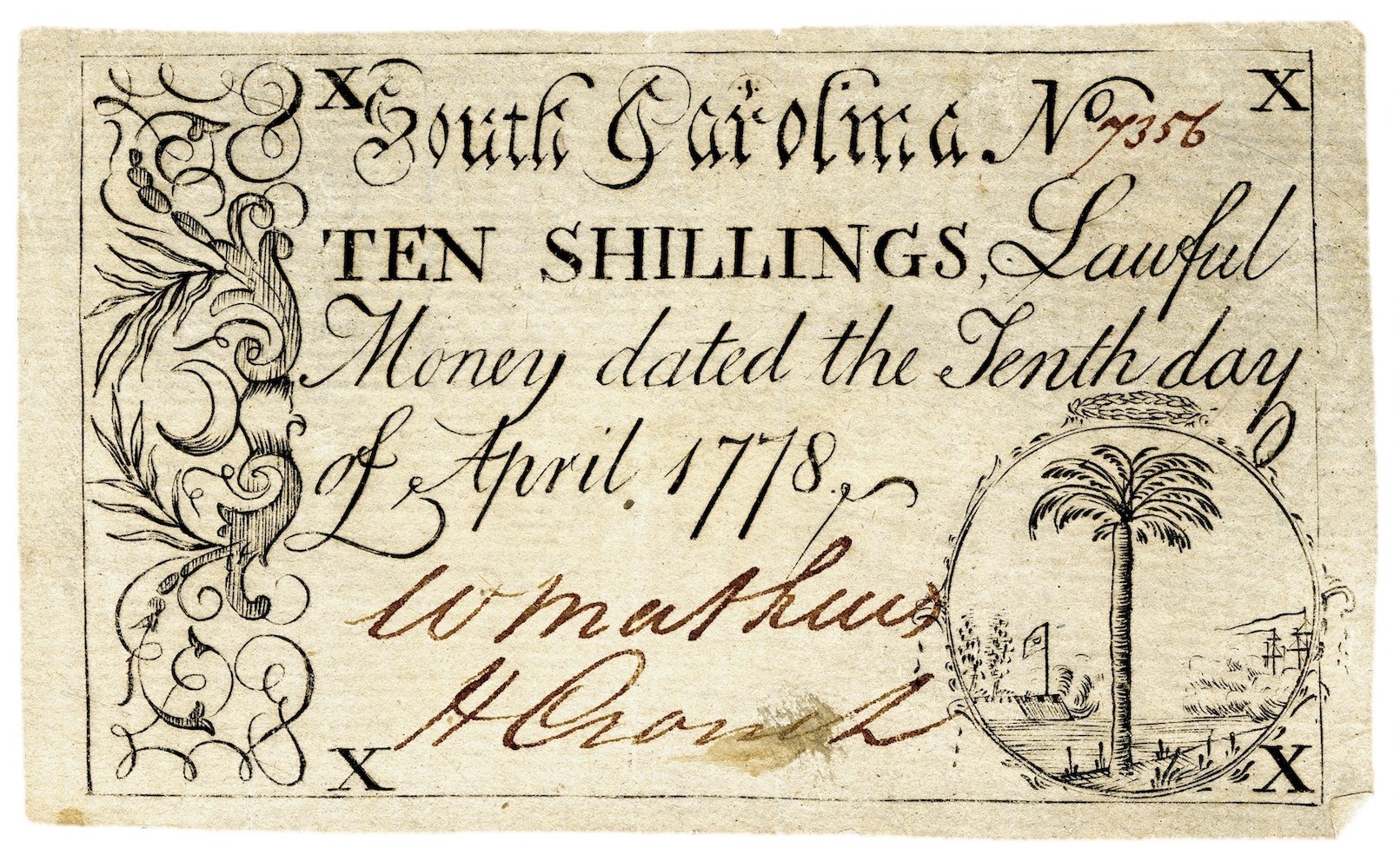

Following the outbreak of hostilities in 1775 between Great Britain and thirteen of its American colonies, South Carolina’s rebellious legislature authorized the emission of new paper currency—still denominated in pounds, shillings, and pence—to sustain its provincial army and to build fortifications. In addition, the nascent state government borrowed money from private citizens and issued interest-bearing receipts or IOUs called “indents” that were transferrable and circulated as money for years. Other rebellious states executed similar financial campaigns, while the Continental Congress in Philadelphia began issuing its own paper notes, called Continental Dollars, that were pegged to the value of the familiar Spanish coin. Owing to the vast number of paper bills circulating within the loose confederation of United States, Americans of the late 1770s witnessed a confusing spiral of monetary depreciation accompanied by rampant price inflation.[2]

Modern readers studying documents produced during the American Revolution can see the hyperinflation of the late 1770s and early 1780s reflected in the large sums of money paid for food, wages, supplies, and loans during that turbulent era. Shortly after American forces surrendered the city of Charleston in 1780, British officials in the capital published a table of depreciation to help local merchants settle accounts contracted during the several previous years.[3] Similarly, the State of South Carolina adopted its own official table of war-time depreciation in the spring of 1783 to facilitate the settlement of local debts contracted between April 1777 and the fall of Charleston in May 1780.[4]

Following the British evacuation of December 1782, the South Carolina General Assembly reconvened in Charleston and began addressing the economic fallout of the eight-year war. Rather than authorizing emissions of new paper money, the state government ratified a law in March 1783 adopting as legal tender the gold and silver coins of various nations already in circulation. A table printed by the legislature denoted the accepted value of crowns and guineas minted by both Britain and France, Spanish pistoles, pistareens, and doubloons, Portuguese Johannes and moidores, and other European coins, the values of which were calculated in relation to the ubiquitous Spanish dollar. To encourage all of these coins to continue circulating in South Carolina, the General Assembly fixed the local value of a Spanish dollar at four shillings and eight pence (£0.4.8) sterling, slightly higher than its contemporary value in Britain.[5]

While the citizens of Charleston and other communities used a confusing array of foreign specie to transact business during the 1780s, the state government settled much of its lingering war debt by issuing multiple rounds of new “indents.” These paper certificates, like the state indents of the 1770s, were essentially receipts or IOUs in various denominations that were transferrable and circulated locally as a medium of exchange. They were not strictly legal tender, however, and were intended to return to government hands in the form of annual tax payments.[6]

The Constitution of the United States, ratified in 1788 and made effective in 1789, reserved to Congress the power “to coin money, [and] regulate the value thereof.” At the same time, the Constitution denied individual states the power to “coin money; emit bills of credit; [or] make anything but gold and silver coin a tender in payment of debts.”[7] Three years later, in April 1792, Congress ratified the first law to establish a Federal mint and “to regulate the coins of the United States.” This coinage act, as it’s commonly known, established the U.S. dollar as the country’s standard unit of money and lawful tender. Its value was pegged, of course, to the familiar Spanish dollar that had circulated among the American colonies for generations. In contrast to the irregular subdivision of the British pound into shillings and pence, the new U.S. dollar was subdivided into decimalized values we still use today—half dollars, quarter dollars, dismes, cents, and milles.

United States coins of various weights and sizes began to flow into South Carolina during the mid-1790s, but many inhabitants continued to record their accounts using the traditional denominations of pounds, shillings, and pence. While surviving newspapers and business records demonstrate that Charleston merchants trading with Britain continued to use such methods well into the nineteenth century, others in the port city patriotically embraced the new national currency. In January 1796, for example, the City Council of Charleston ratified an ordinance declaring that henceforth all public accounts in the city “shall be kept in dollars, cents, and milles.” Neither the state nor the city government required private citizens to use the new currency, but City Council expressed its hope the law would “induce our fellow citizens to follow the example in their different transactions.”[8]

The paper bills and foreign coins that circulated across South Carolina during the eighteenth century faded from local memory after the turn of the nineteenth century, but citizens of the United States continued to profit from the financial acumen that evolved during the nation’s colonial infancy. Generations of experience using credit to conduct trade both locally and internationally facilitated the rise of banks and major corporations during the early years of the Industrial Revolution. In many respects, we can see the roots of our increasingly cash-less, global economy in the creative accounting practices improvised by the economic pioneers of centuries past. The knowledge we gain from this financial review illustrates the value of studying history: We can leverage the past to help us evaluate the present and speculate on the future.

Suggestions for Further Reading:

- Anonymous. An Essay on Currency, Written in August 1732. Charleston, S.C.: Lewis Timothy, 1734.

- Bull, William. “An Account of the Rise and progress of the Paper Bills of Credit in South Carolina from the year 1700 to this present time, together with the computed value, in money of Great Britain, of such bills, at the respective times of their creating and issuing, and the value of such bills in money of Great Britain at this time; and also, an account of the rates and prices of gold and silver coin in the province of South Carolina, in the years 1700, 1710, 1720, 1730, and at this present time” [1740]. In The Statutes at Large of South Carolina, volume 9, David J. McCord, ed., 765–80. Columbia, S.C.: A. S. Johnston, 1841.

- Coclanis, Peter A. The Shadow of a Dream: Economic Life and Death in the South Carolina Low Country, 1670–1920. New York: Oxford University Press, 1989.

- David, Huw. Trade, Politics, and Revolution: South Carolina and Britain’s Atlantic Commerce, 1730–1790. Columbia: University of South Carolina Press, 2018.

- Grubb, Farley Ward. The Continental Dollar: How the American Revolution Was Financed with Paper Money. Chicago: University of Chicago Press, 2023.

- Jellison, Richard Marion. “Paper Currency in Colonial South Carolina, 1703–1764.” Ph.D. diss., Indiana University, 1953.

- Jellison, Richard M. “Paper Money in Colonial South Carolina: A Reappraisal.” South Carolina Historical Magazine 62 (July 1961), 134–147.

- McCusker, John J. How Much is That In Real Money? A Historical Commodity Price Index for Use as a Deflator of Money Values in the Economy of the United States, second edition. Philadelphia: American Antiquarian Society, 2001.

- McCusker, John J. Money and Exchange in Europe and America, 1600–1775: A Handbook. Chapel Hill: University of North Carolina Press, 1978.

- McCusker, John J., and Russel R. Menard. The Economy of British America, 1607–1789. Chapel Hill: University of North Carolina Press, 1985.

- Nettels, Curtis. “The Origins of Paper Money in the English Colonies.” Economic History 3 (January 1934): 35–56.

- Perkins, Edwin J. American Public Finance and Financial Services 1700–1815. Columbus: Ohio State University Press, 1994.

- Ramsay, David. “Fiscal History of South Carolina, from 1670–1808,” in The History of South Carolina, volume 2, pages 163–198. Charleston, S.C.: David Longworth, 1809.

- Smith, W. Roy. “Financial History,” in South Carolina as a Royal Province 1719–1776, pages 228–329. New York: Macmillan, 1903.

- Thayer, Theodore. “The Land Bank System in the American Colonies.” Journal of Economic History 13 (spring 1953): 145–59.

- Woods, Michael. “The Culture of Credit in Colonial Charleston.” South Carolina Historical Magazine 99 (October 1998): 358–380.

[1] See Section 8 of Act No. 957, “An Act for granting to his Majesty the sum of sixty thousand pounds, for the building [of] an Exchange and Custom House, and New Watch House, in Charlestown, for the service of this government, and for other services therein mentioned, and for appointing and impowering commissioners to execute the same,” ratified on 18 April 1767, in Thomas Cooper, ed., The Statutes at Large of South Carolina, volume 4 (Columbia, S.C.: A. S. Johnston, 1838), 257–61.

[2] For an overview of the fiscal history of the war years, see David Ramsay, The History of South Carolina (Charleston, S.C.: David Longworth, 1809), 171–83.

[3] South Carolina and American General Gazette, 30 December 1780, No. 1127, page 1: “This Day is published, price, one dollar, and to be sold at Wells’s Book Store, No. 71, Tradd street, An Accurate Table, ascertaining the progressive Depreciation of the Paper-Currency in the Province of South Carolina, during the late Usurpation; with a comprehensive Digest of the Proofs and Evidences, laid before the Commissioners appointed for that Purpose, by the Hon. James Simpson, Esq; Intendant-General of the [Board of] Police in the said Province; whereon the said Table is founded: To which are subjoined, a few brief Observations, tending to elucidate so intricate a Subject.”

[4] Act No. 1185, “An Act for settling a depreciation table,” ratified on 16 March 1783, in Cooper, Statutes at Large of South Carolina, 4: 563–64.

[5] Act No. 1162, “An Act to ascertain the weight and value of the several gold and silver coins in circulation in this state; and to punish persons who shall counterfeit or utter or attempt to pass the same, knowing them to be counterfeit,” ratified on 12 March 1783, in Cooper, Statutes at Large of South Carolina, 4: 542–43.

[6] For a description of the post-war indents, see Ramsay, History of South Carolina, 2: 183–98.

[7] See Article I, Sections 8 and 10 of the U.S. Constitution.

[8] “An Ordinance to regulate the manner of keeping Public accounts within the City of Charleston,” ratified on 16 January 1796, in Alexander Edwards, comp., Ordinances of the City of Charleston (Charleston, S.C.: W. P. Young, 1802), 137–38. Note that this ordinance went into effect on 1 February 1796.

NEXT: Surf Bathing at Sullivan’s Island in the Early 19th Century

PREVIOUSLY: Phebe Fletcher: A ‘Magdalene’ in Revolutionary Charleston

See more from Charleston Time Machine